The Buy-and-Build Playbook: Why Private Equity is Deploying Billions into Electrical Contractors

July 17, 2026

At A Glance

The thesis for investing in commercial and industrial service platforms has evolved. No longer viewed strictly as cyclical sub-contractors, electrical contracting platforms have emerged as premium, highly strategic assets. For private equity investors and portfolio operating partners, the sector offers a rare combination of recession-resistant operational demand, secular macro tailwinds, and extreme market fragmentation perfect for explosive buy-and-build execution.

HOW WE DEFINE ELECTRICAL CONTRACTORS

Within a sophisticated investment thesis, Electrical Contractors are defined far beyond basic wiring. They provide the critical installation, lifecycle maintenance, regulatory repair, and digital modernization of power and data architecture across residential, commercial, industrial, and institutional markets.

Modern platforms specialize in a complex matrix of technical services, including:

-

High-voltage power distribution and grid-edge integration.

-

Advanced automation, SCADA controls, and industrial instrumentation.

-

Low-voltage systems, mission-critical fiber optics, and smart-building systems.

-

Renewable energy systems, on-site microgrids, and EV fleet charging hubs.

-

Predictive infrastructure testing and non-discretionary preventative maintenance.

These platforms operate as the literal life support systems for the broader construction and facility services ecosystem. They are essential partners for institutional asset owners, large-scale general contractors, and global facility operators.

Historically, revenue models heavily favored lump-sum, project-based construction. Today, the most valuable market leaders drive value through blended revenue models. They anchor their financials with high-margin Master Service Agreements (MSAs), recurring preventative maintenance contracts, and rapid-response emergency services.

Furthermore, leading sponsors are aggressively expanding these platforms horizontally into diversified MEP (Mechanical, Electrical, and Plumbing) powerhouses. This consolidation strategy locks down multi-trade cross-selling opportunities and cements unbreakable, single-source enterprise customer relationships.

WHY PRIVATE EQUITY IS INVESTING HEAVILY IN ELECTRICAL CONTRACTORS

The rush of institutional capital into this sector is driven by an airtight alignment of macroeconomic tailwinds and highly predictable operational playbooks.

Exposure to Infrastructure and Construction Growth

Platform companies are capturing massive tailwinds from continuous, multi-billion dollar capital allocations into grid modernization, healthcare infrastructure, and institutional facility retrofits. Secular demographic shifts and a rapidly aging domestic grid ensure that large-scale infrastructure upgrades remain entirely non-discretionary, sheltering these businesses from standard real estate cycles.

Fragmented Market with Significant Consolidation Opportunities

The North American landscape remains hyper-fragmented, characterized by thousands of localized, founder-owned entities facing imminent succession cliffs. This structural dynamic gives PE firms a highly repeatable multiple-arbitrage playbook. Sponsors can aggregate lower-middle-market tuck-ins at lower valuation multiples (4x–6x EBITDA) and instantly roll them into a unified regional platform commanding premium institutional multiples (10x+ EBITDA) via scale, shared corporate services, and expanded geographic depth.

Growing Demand for Skilled Technical Services

Modern facilities demand unparalleled technical sophistication. Complex automated logistics centers, energy management software, and high-voltage systems require specialized, certified technical labor. This deep technical barrier to entry protects incumbent platforms against low-cost competitors, yields strong pricing power, and sustains premium gross margins.

Recurring Revenue Through Service and Maintenance

The shift toward an asset-light, service-first operational mix is the ultimate value lever for PE investors. Long-term facility support contracts, mandated safety inspections, and mission-critical system repairs produce reliable, recurring cash flows. This counter-cyclical revenue base provides an exceptional financial floor, mitigating downside exposure during broader economic contractions.

Data Center and Industrial Expansion

The meteoric rise of generative AI, high-density cloud computing, and advanced manufacturing nearshoring has triggered an unprecedented boom in specialized facility construction. Electrical contractors capable of building out hyper-scale data centers or battery gigafactories secure highly lucrative, multi-year contracts with top-tier technology and industrial developers, driving enormous backlog visibility.

Value Creation Through Operational Improvement

Sponsors unlock massive operational arbitrage by institutionalizing founder-led businesses. Portfolios rapidly drive margin expansion by implementing enterprise resource planning (ERP) systems, professionalizing talent acquisition to combat the skilled labor shortage, optimizing project bidding algorithms to stop margin slippage, and automating field-service dispatching.

THE NUMBERS

The institutionalization of this sector is well underway, reflecting deep sponsor commitment to the fragmented trade services space:

-

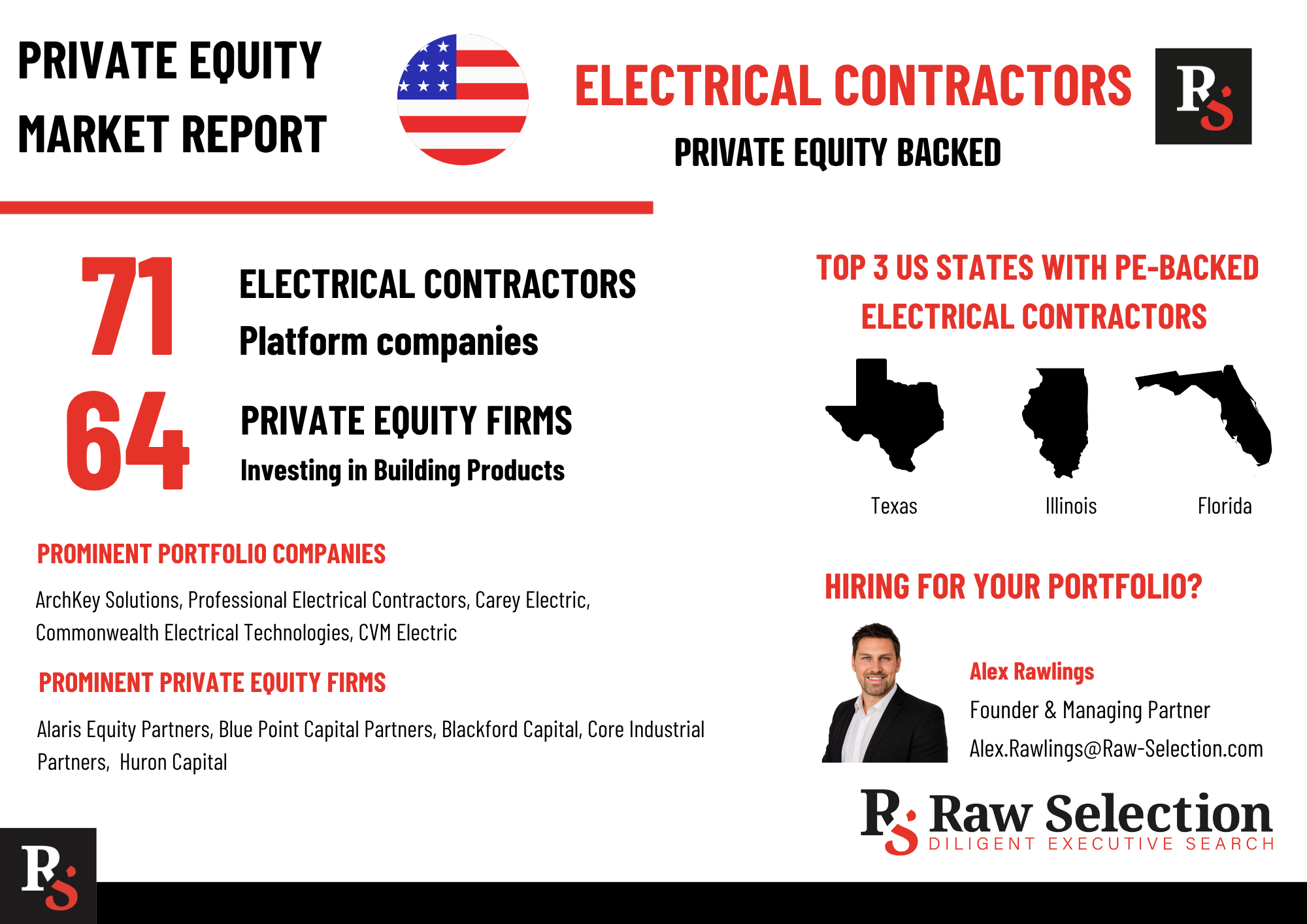

Total Active Platform Companies: 71

-

Total Private Equity Firms Actively Investing: 64

Note: These figures capture platform investments only, completely excluding the hundreds of confidential bolt-on and tuck-in acquisitions executed by these platforms annually to expand regional density.

PROMINENT PORTFOLIO COMPANIES

Several highly active PE-backed platforms illustrate the successful execution of regional and national scale strategies in the current market:

-

ArchKey Solutions: A dominant national powerhouse executing complex commercial, industrial, and mission-critical data center projects across the United States. In a landmark sector shift, global asset manager 26North Partners completed its high-profile acquisition of ArchKey, underscoring immense institutional interest in scaled electrical assets.

-

Professional Electrical Contractors (PEC): A premier diversified provider optimized to deliver programmatic specialty rollouts, large-scale commercial retrofits, and comprehensive industrial system installations.

-

Commonwealth Electrical Technologies (CET): A recognized market leader focused on complex infrastructure projects, utility modernization, and high-performance commercial construction.

-

CVM Electric: A specialized, full-service contracting platform built to deliver institutional-grade engineering and electrical automation across complex commercial and institutional end markets.

-

Pinnacle MEP: A fast-scaling multi-trade platform that perfectly executes the integrated mechanical, electrical, and plumbing thesis across highly resilient commercial verticals.

PROMINENT PRIVATE EQUITY FIRMS

The following middle-market and upper-middle-market private equity sponsors have established dedicated investment theses in the skilled trades, field services, and facility infrastructure sectors:

-

Alaris Equity Partners – Known for strategic growth capital structures in resilient service models.

-

Blue Point Capital Partners – Highly active in standardizing operations and expanding regional scale for lower-middle-market industrial platforms.

-

Core Industrial Partners – Heavily focused on technical manufacturing and industrial technology-adjacent contracting services.

-

Blackford Capital – Specializes in driving professionalized operational playbooks in founder-led manufacturing and specialty trade platforms.

-

Huron Capital – Renowned for its repeatable "ExecFactor" buy-and-build playbook across facility, infrastructure, and commercial services.

TOP STATES FOR PE-BACKED ELECTRICAL CONTRACTOR COMPANIES

Sponsor investment density directly matches regional macroeconomic strength. The heaviest concentrations of PE-backed platforms are strategically localized in:

-

Texas

-

Florida

-

Illinois

These dynamic states serve as major geographic anchors because they benefit from high populations, aggressive commercial development, state-level infrastructure funding, and immense expansion across the manufacturing, logistics, clean energy, and data center corridors.

LOOKING AHEAD

Moving forward, the electrical contracting sector will remain an exceptional alpha-generating asset class within commercial and industrial services. As institutional facilities face an increasingly digital and electrified future, the demand for highly sophisticated contractors will only accelerate.

Private equity sponsors will continue to aggressively hunt for targets. Expect premium multiples to be commanded by assets that boast a high percentage of non-discretionary service revenue, possess highly specialized automation or high-voltage technical capabilities, and demonstrate a repeatable playbook for seamlessly integrating smaller geographic tuck-ins.

Get in Touch

Raw Selection favors a meticulous approach to talent research. Our process for selecting the right talent means we can boast a 100% success rate for all our retained and engaged C-Suite clients, with 96% of placed candidates still in their roles after 12 months.

If you are looking for new talent, contact us now.